Alchemist's Weekly Strategy Notes

Alchemist's Weekly Strategy Notes

Be mindful of the tail risk, but don't let near term volatility shake you out

Besides to strong start to the year in Q1, the biggest inflection point in my mind for this year was the FOMC meeting on March 20, 2024. Whether we agree with Powell’s stance or not, he made it quite clear that he is itching to cut. Just as last year’s consecutive decline in inflation did not catalyze him to rush into cutting, this year’s hotter than expected inflation in the start of the year did not catalyze him to panic and abolish his stance on believing that rates have peaked and that we will commence the cutting cycle later this year.

See my last week’s post (Mar 27) where I walk through FOMC meeting recap in depth

Let’s not forget the year has still been very strong

After the strong Q1 we had in equities (where SPX is up 10 %, SOXX +21 %, NDX +10%), it is natural we have some profit taking, especially where valuations are richer. When talking to large hedge funds in the biotech space, for instance, many folks are up more than 20-25% in the quarter alone. After a rough 2-3 years in biotech, these PMs don’t want to be too greedy and ungrateful of the rally we saw in these higher beta smaller cap sectors. This market is extremely momentum driven. Even though people are feeling anxious with a couple days of correction, let’s not forget risk-on assets already had an incredible start to the year. One doesn’t have to search far to see the most speculative sector at all, cryptocurrencies, where Bitcoin +50% and other major altcoins like Ethereum, Solana, and even some meme coins rally 10x+ (though these are highly illiquid, highly influenced by leverage and much smaller market cap). Regardless, it serves as a quick reminder to zoom out and realize for some key sectors, it has been a banner start to the year.

So where do we go from here? How do we digest the incoming economic data?

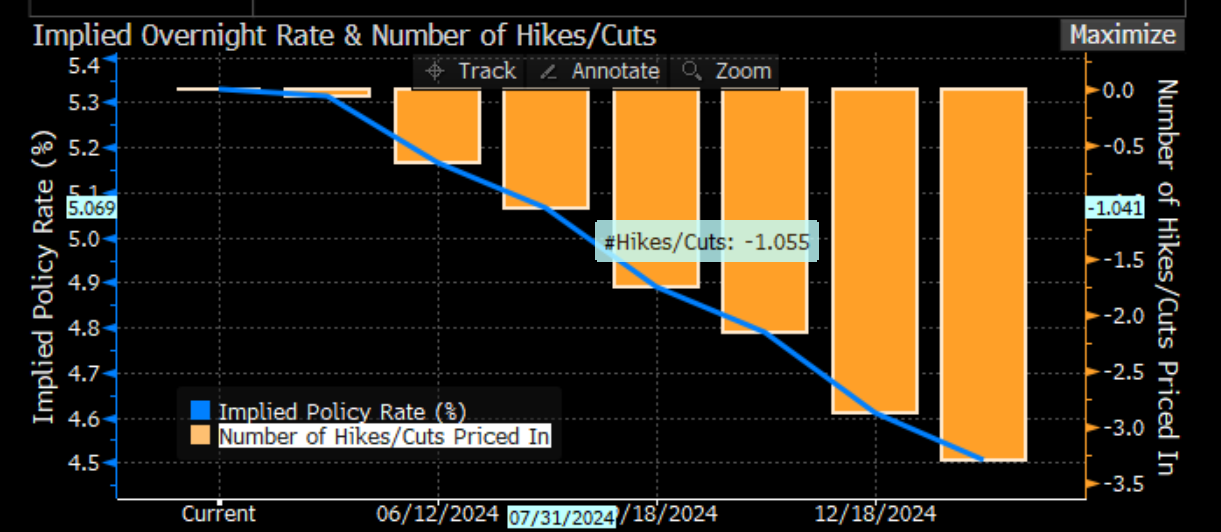

Now, undoubtedly in our current position, the risk/reward of certain investments and trades have certainly changed. Post-FOMC, despite Powell’s dovish stance, the market has to endure the continual release of macroeconomic data that will constantly shift interest rate expectations which will, consequently, affect short-term volatility and price action. How traders, investors and market participants express that expectation is actually a probability that we see here below:

First cut expected to come in July now

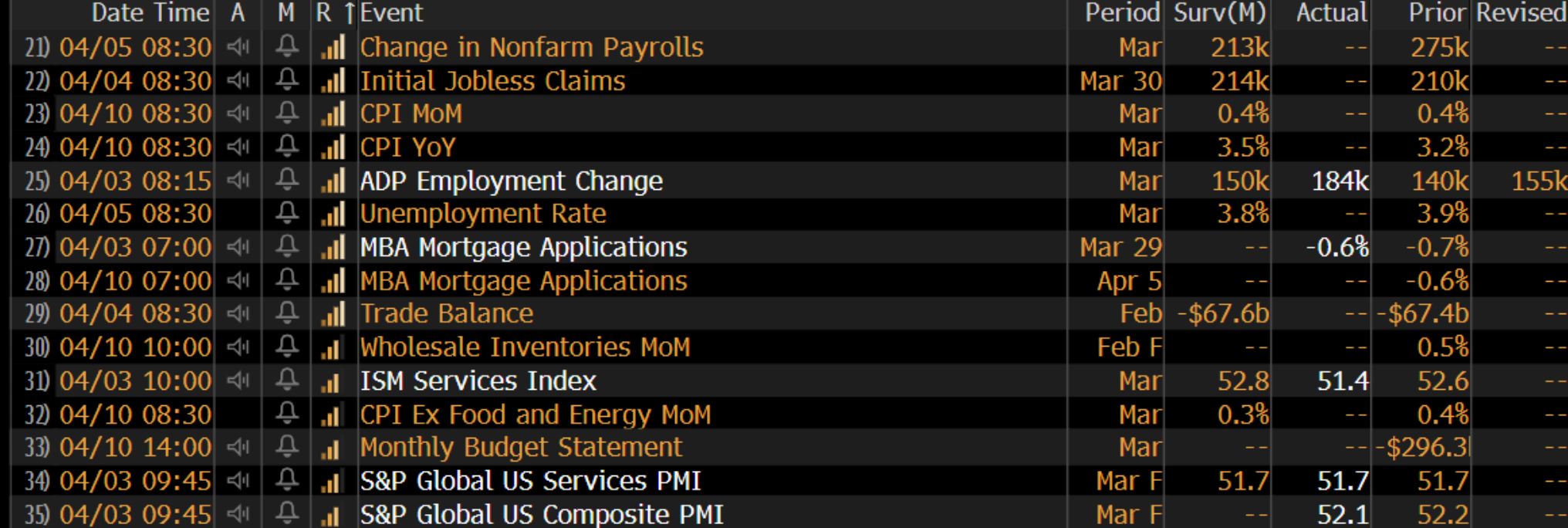

The two pieces of key economic data that were market moving since Powell’s clear stance were (1) PCE data (Fed’s favorite barometer) and (2) PMI. PCE is largely in line with expectations and given Powell’s clear stance of wanting to cut, data would have to be quite hot before there is an issue to walk back. PMI was an interesting one. (PMI is a leading indicator for economic health as it surveys how Purchasing Managers rate the relative business conditions including production employment, new order, inventories, deliveries, etc.) We had a reading above 50 (50.3 to be precise), which is much higher than the forecasted 48.5, so given how short-term this market is and how positioning is stretched, it is not too much of a surprise that we are experiencing some correction. Looking longer term, though, I actually find this PMI great news as it debunks one of the biggest, bearish hurdles of all, recession fears. Today’s Wednesday ISM numbers coming in lower also helped bring the markets back to green…

Important Market moving economic data

Tactical Plan to go from here

Zooming out of all this near-term volatility and market choppiness from every economic data point and every Federal reserve comment, as long as we get no out of line inflation surprises, the path remains the same in terms of staying long. Powell has made it clear so far.

To best take advantage of this current market set up, I would be positioned long into two core buckets, (1) high quality, large cap thematic growth names and (2) take advantage of market beta from rate-sensitive high growth smaller caps.

The conservative bunch will continue accumulating into $TLT and longer duration bonds, but for my taste, I don’t think it is the best risk/reward from an IRR perspective. Reason being is that in the near term, we still have all these data releases and commentary that move rates around (just take a look in the rise in rates this past week alone that have even retraced the rates drop post-the FOMC meeting). Lastly, even if it were to drop, the cuts would be more gradual.

On the contrary, you are better off holding buckets (1) and/or (2). For bucket (2), if we get a drop in the 10yr, high beta small caps, Russel2000, biotech, cloud, even crypto etc. should all rally much more significantly in anticipation of the cycle commencing. These assets will mean revert. On bucket (1), AI/semiconductors, large caps, and thematic biopharma names, all have been rallying despite the fluctuation in rates. Though P/E’s have inched up, their robust cash generation engines and rate insensitivity will allow you to continue to compound in the short-term AND long-term, given we believe the long-term trend is bullish. If you were to be more aggressive and tactical, one can shift from bucket (1) to bucket (2) as we get closer clarity to a rate cut. If you were a longer term investor, a portfolio of these two core baskets should serve you well this year. (Will have a more detailed post coming up to detail the specific themes)

Let’s take a look at our key charts for this week.

Key Dashboard Charts

1.) How cheap (or expensive) are stocks?

The majority of S&P500 stocks are all trading well above their 50 and 100 day moving averages, indicating equity prices are certainly not cheap from a technical perspective. Nasdaq is a bit weaker but not obviously oversold from a technical lens. VIX is within the expected range and there aren’t any crazy spikes in put/call ratio. We are in grind mode in the markets.

2.) All-in-one Chart (Market Drivers in this Macro Regime)

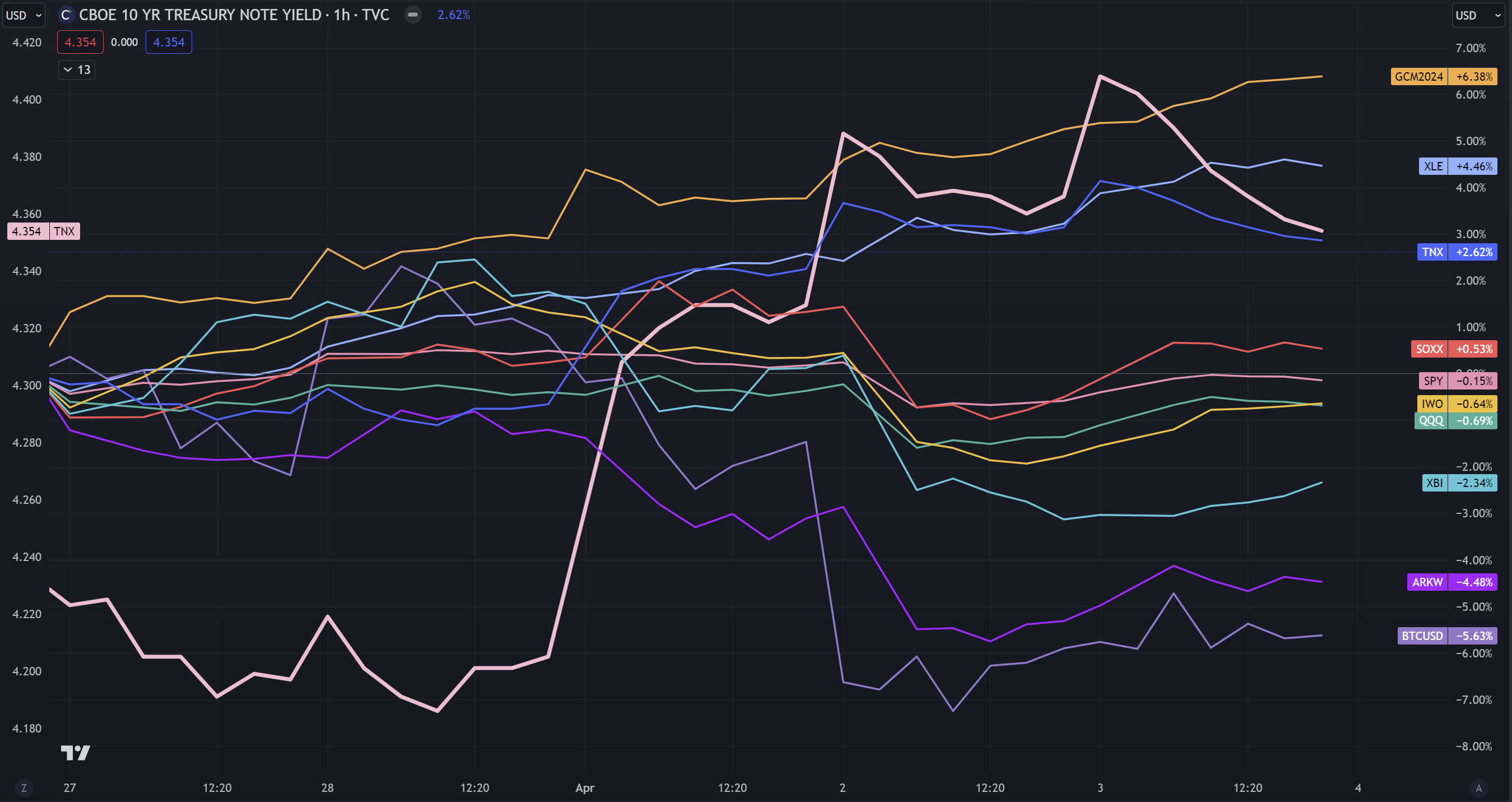

The rise in rates, DXY and Oil has been steady upwards, however S&P500 has been relentless. Ever since the start of the year, the market stopped caring about rates. When will this break… or have we just seen past this?

3.) What sectors have been outperforming in the past week

Clear outperformance from Gold, Oil and 10yr yield continuing to inch up. All 3 ingredients that are not great for risk-on assets.

4.) Deeper look at how rates affected equity prices

We have reversed all the rate decreases post-Fed’s FOMC meeting. Most equities have been lower since meeting despite the dovish talk, except Russel 2000.