Alchemist's Weekly Strategy Notes

Alchemist's Weekly Strategy Notes

Resilient as Hell. NVIDIA carried the market yes, but it also takes a village.

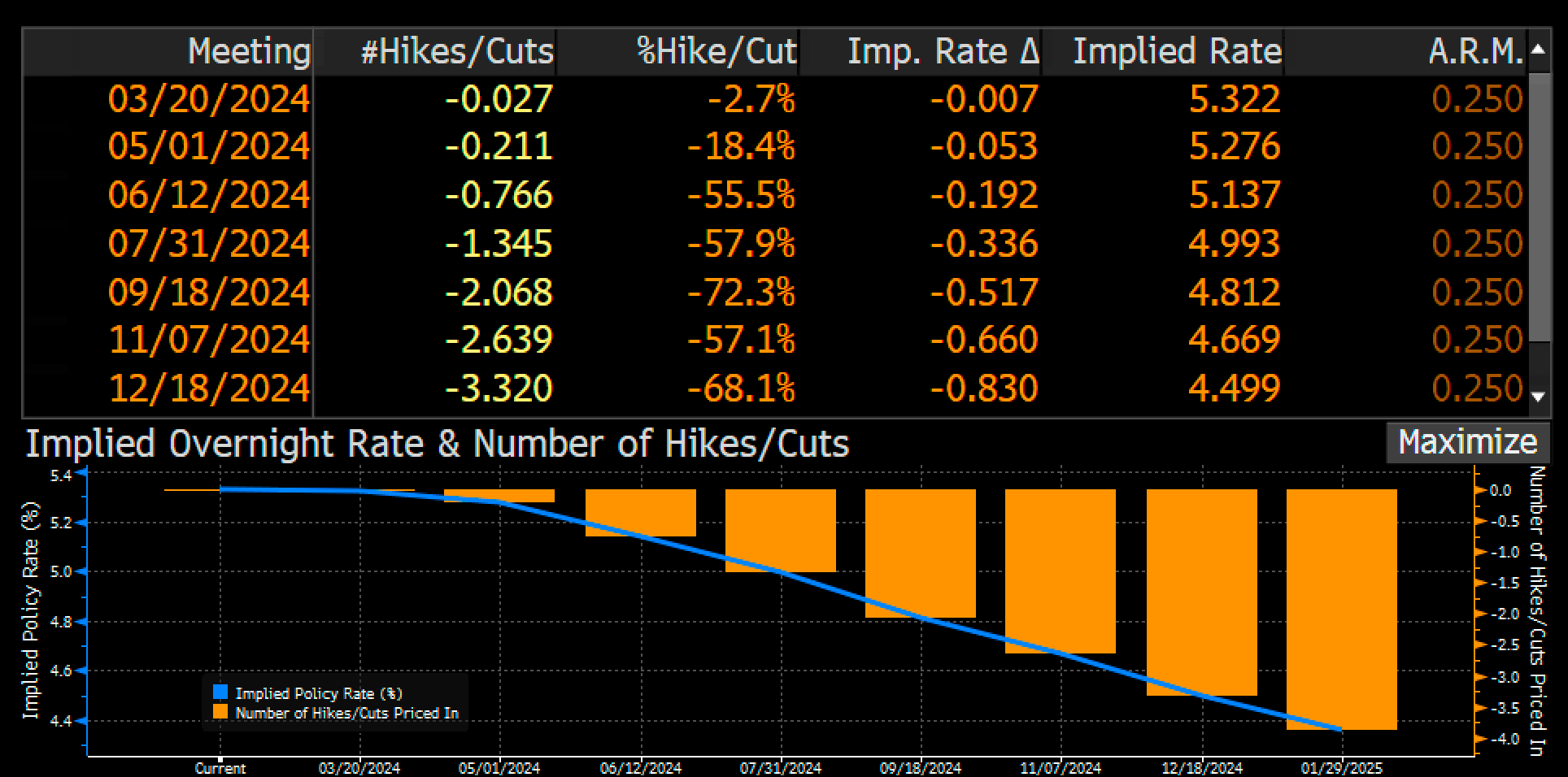

One of the most obvious conundrums that have plagued many bears and bulls is how resilient this market is. The place where this is the most obvious is looking at rates. In recent months, the stock/long-duration rates inverse correlation has fell apart. Despite the fact we have gone from 7 cuts this year to 3 to maybe 1 (and some outlier hawks calling for 1 more hike…) the market has continued to rally. The thesis we have been talking about still stays in tact, without burying the lede continue to be long and strong in quality and thematic bets. The one point of weakness we saw was in mid Feb when we had a hotter than expected CPI, but the market quickly shrugged that off because (1) we thought it might be an anomaly (this is harder to prove) or (2) a hotter CPI means the economy is still very strong. OK maybe no cuts in March or even May, but that’s okay because there won’t be a recession in the near term.

That said, this rally has been intoxicating, as semiconductor indices like SMH and SOXX have flirted with 15-20% gains in just 2 months, QQQ +10%, etc. This is strength like no other, especially even after a strong Q4 2023. Where is this strength coming from? As a fundamental long-term investor, I can say that though there are some crazy hype names in AI like those of SMCI and ARM, etc. the market overall in the quality megacaps that have carried the market are actually not in bubble territory. In fact, in many cases their P/E are lower now than that of 2021, because earnings have just grown so tremendously. It is this fundamental business growth that trumps all macro, technical and sentimental fears.

So NVDA carried the market and the sentiment, but it takes a village to win. At least in the case of the megacaps, in Q4, the Magnificent 7 grew sales by +15% year/year and lifted margins by 607 bps year/year, leading to earnings growth of 60%. In contrast, the remaining 493 stocks in the S&P 500 grew sales by 3% year/year while margins contracted by 59 bps, such that earnings fell by 2%. +60% vs -2%. +60% earnings growth in the top names that make up a majority of the index. This is not a bubble. This is fundamental strength in the monopolistic leaders in the market. How sustainable is this, how much further can we go? That is a separate topic. But the footing we are on now is on pretty solid foundation. And NVDA? Well, NVDA has added around $1.7 TRILLION of market cap over the past 16 months, and the P/E has not moved, so from a valuation standpoint its multiple is actually very sensible. Lower P/E than many unprofitable names in the Russel 2000…

Furthermore these megacaps have some of the best balance sheets in the world and invest 60% of their cash flow in R&D and acquiring competitors. Not to spend too much time on business strategy and money as a competitive edge, there is an element that these behemoths have annual innovation budgets they can burn that is larger than most market companies and competitors. All this taking in sum, it becomes less perplexing why rates not budging has no effect on the broader market, esp. one that is so concentrated in these leaders.

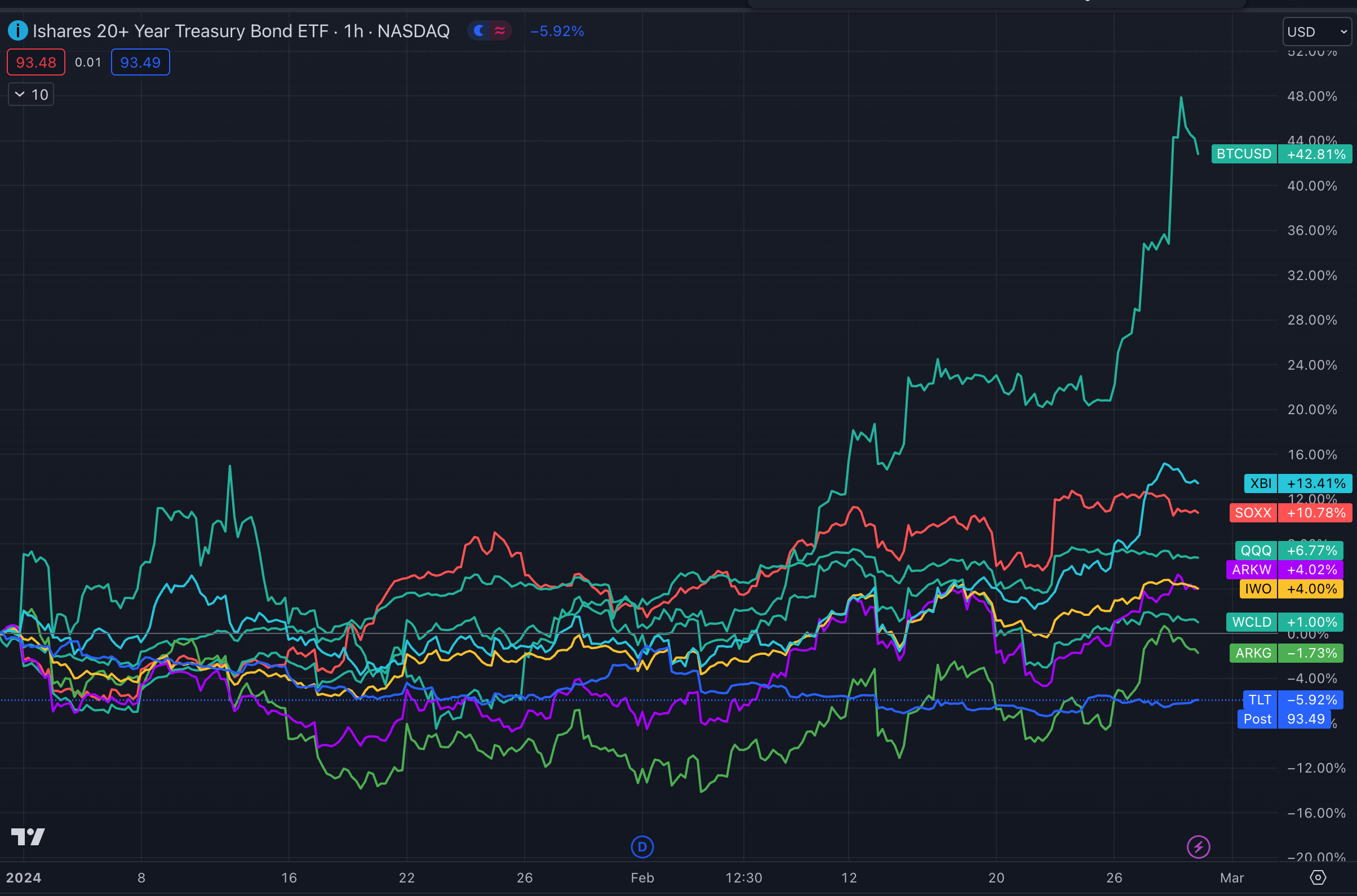

In mid-January, the interest rate market predicted 167 basis points of Fed easing for the year, with the S&P closing at 4783. Now, that expectation has dropped to 82 basis points, but the S&P closed at 5087. While this oversimplifies things and overlooks factors like the impressive performance of mega-cap tech stocks, it emphasizes that the stock market can thrive without relying solely on adjustment cuts. (On the tactical side, the call that many and their mom made regarding going long TLT didn’t actually pan out, as you would have been just better off longing equities. In fact TLT has kept bleeding as rate cuts get pushed out while the fundamental outperformance of amazing businesses just carry equity prices up).

In fact, it seems like even small cap rate sensitive assets don’t seem to care that rates have been stuck in a range / creeping up. TLT continues to bleed (as long duration rates trends upwards and chops) as small caps outperform and some even break out of their long term ranges. XBI (the biotech index) is a great example of this and deserves a much longer write up.

PCE data is tomorrow, which should be another very important data readout for inflation. Weakness today probably can be explained by the usual taking risk off the table before an impending data readout since the market is so inflation expectation sensitive. In contrast to the earlier emphasis on the six-month annualized rate of core PCE inflation and Chair Powell’s indication that cuts should come “well before” inflation reaches 2%, Fed officials now appear to be taking a more cautious approach of wanting more definitive evidence that inflation will approach 2% before cutting, in part because some worry that the stronger performance of the economy could inhibit further progress in reducing inflation.

At these levels, though risk/reward gets less and less favorable, though the longer term trend for the year still looks bullish given (1) fundamentals, (2) potential rate cuts, (3) market liquidity. The big risk of course, as we just mentioned is if inflation keeps surprising to the upside. That would be a problem for all risk-assets.

Despite crypto chatter being eerily quiet this time around, no other evidence needed of a bull market or at bare minimum the liquidity and euphoria in the markets than to see the amazing run up in crypto. We are flirting with BTC all-time highs and Coinbase’s exchange even crashed as they were overloaded with users.