Alchemist Weekly Strategy (Bracing for a healthy cooldown)

Regardless Bull or Bear, Moderating exposure seems rational, especially as we enter election period.

We have covered many important themes in recent posts regarding megacap EPS growth dominance, software’s cheap valuation metrics and the disconnect from the AI beneficiaries, importance of macro data, etc. All those themes remain true. This post will be shorter as I think not much has changed recently and all eyes will now be focused on the start of earnings season. I am still constructive and bullish in the longer term, but the short answer is that this is NOT the time I would be adding exposure. Consolidate down to high quality and trim exposure on lower conviction names. Ultimately this next week will face CPI/PPI data this Thursday/Friday which would be extremely important. Powell will also speak on Tuesday.

Fundamentally, a lot of the recent move up in semiconductor stocks have been driven by multiple expansion vs. earnings growth. Semis are still a highly strategic and bullish sector but I would not be adding net new large positions at these values. (Longer term holds are fine.) On software, valuation multiples are at historically cheap multiples. Risk/reward will be better here scaling in vs. semis at this current juncture. Though given the current setup in the markets, there are still headwinds in terms of software guidance getting pared back and enterprise software getting cut and diverted to AI capex spend.

If you are looking at fund flows and seasonality, backed by 50+yrs of trading data from prime brokerages, the market tends to peak around mid to late July. After that, August, September and October tend to be weaker months. You may recall the exact technical bottom of the most recent bear market correction was October 14, 2022. The semis index is up more than 160%+ and the NASDAQ-100 almost +90% since then!

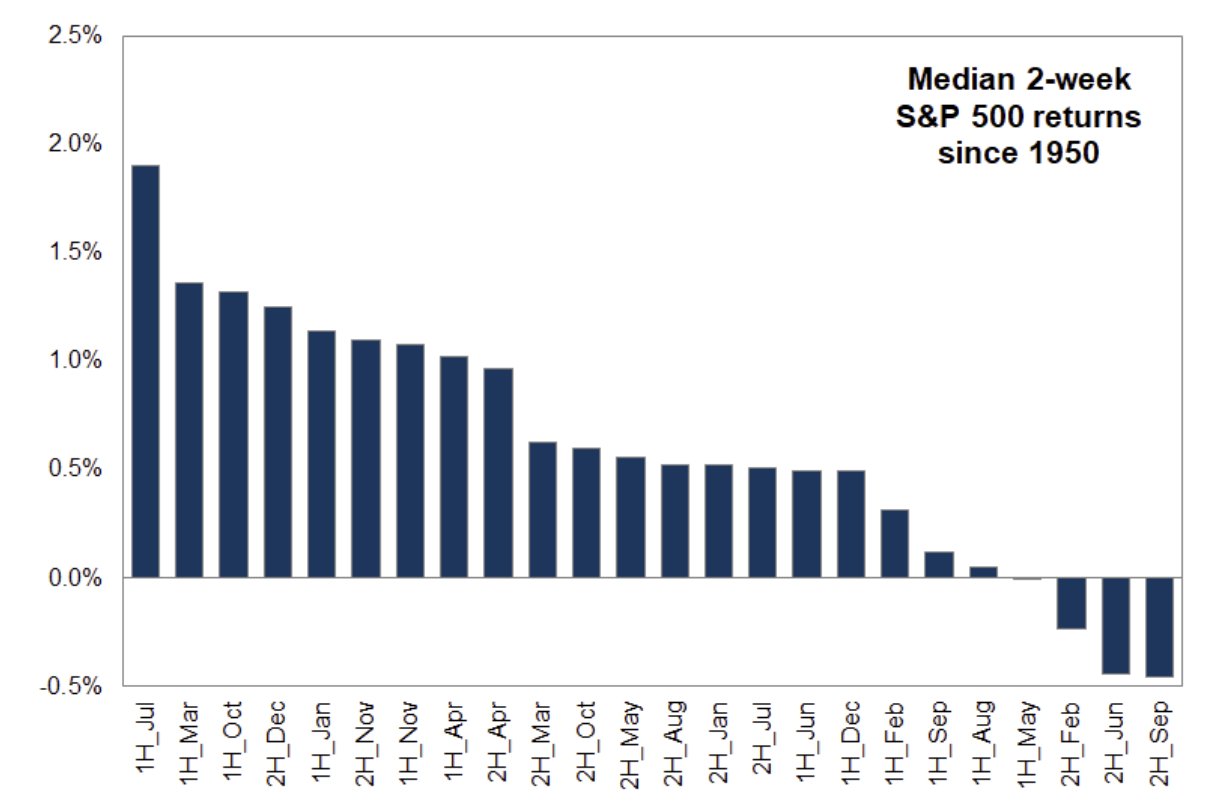

With an incredible first half of 2024 with almost +20% and +25% run in the S&P500 and NASDAQ respectively, as we head into a (1) steeper multiple expansion with higher expectations for earnings, (2) seasonally weaker time period in Aug-October, (3) election cycle, I think it makes sense to be ready for a correction. History has shown us many years where the market can end up being up big, but largely be dead money or significantly down between the summer and early fall months. 2H of September is among the worst. August is the month with the largest outflows of the year from equity passive and mutual funds. August is typically the largest month of the year for outflows as allocations are full.

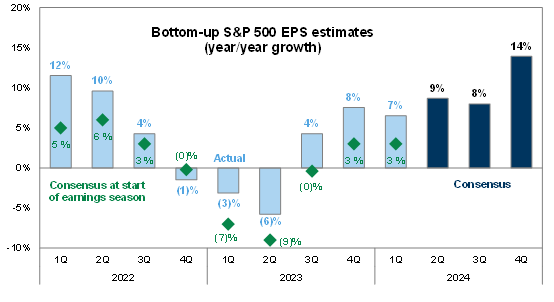

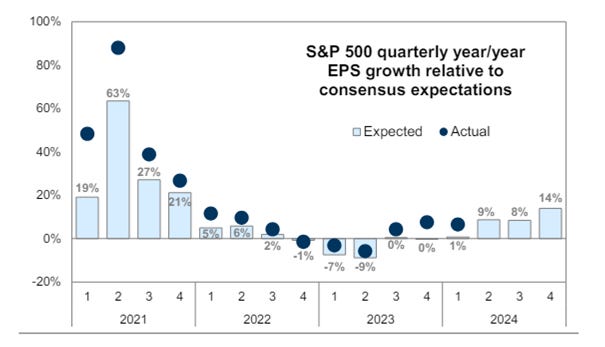

(1) If you look at the bar for bottom-up S&P500 consensus EPS estimates they are meaningfully higher than the past 2 years. Given the consistent beat of earnings, the start of season consensus is quite high for the back half of the year.

(2) You can see here clearly that we are just approaching a seasonally weaker period in general. It doesn’t help too much that CTA’s are positioned near the top of the range.

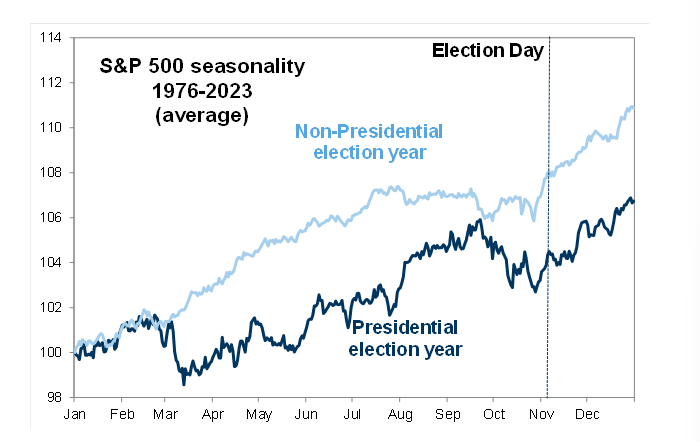

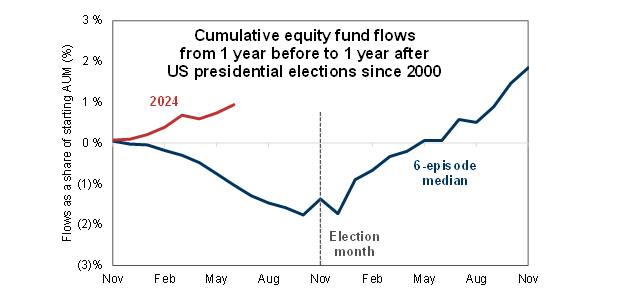

(3) In addition to elevated positioning levels and poor seasonality closer to the fall, election year typically sees heightened positioning and volatility leading up to an election. This set up in general signals that there may be buying opportunity closer to October and November time period.

A quick review of the everything chart, you can see that the macro picture (which we will get important data later this week) still stands. The falling rates have been a catalyst for S&P500 higher. Crude, however has been inching up higher in its range, so that is important to keep an eye on in terms of how it affects inflation data.

Taking a look at the breadth measures of the broader markets, the S&P500 sector as a whole has actually been weaker than expected given that S&P500 keeps breaking new all time highs after all-time-highs. NDX is a bit stronger, but in both cases, if you just look at the market internals, it doesn’t look like a record high index. Again, the concentration in the haves vs. have nots continue. Until we get more macro clarity and rate cuts, I expect many of these names to continue to chop. That said, this snapshot is important to look at to understand how heated internals are.

Lastly, taking it back full circle, the market is very complacent right now. VIX is at the lows of the range, Put/Call ratio is a the lows of the range. Most people are sitting comfortably long in their positions with minimal hedging. This is particularly the time you would want to buy insurance when you don’t feel like you need to.

That’s a wrap for this week. Stay tuned for CPI/PPI data to see signs for hopefully cooling inflation prints, which should support the markets. Other than that, we are kicking off earnings season where expectations are higher than they are usually, so there is no easy free lunch. Companies will have to deliver.